值得关注的趋势

[加拿大铁路罢工]

- 在加拿大劳资关系委员会(CIRB)于 8 月 9 日(星期五)做出裁决之前,由卡车司机工会(Teamsters Union)代表的近 10,000 名加拿大铁路工人可能会在下周初举行罢工。

- The dispute involved the Canadian National Railway Company (CN) and Canadian Pacific Kansas City Limited (CPKC), over issues related to working conditions, wages, and fatigue management.

- Canadian railways transported half of the country’s exports in 2022, totaling more than $276 billion dollars’ worth of goods, according to the Railway Association of Canada.

- A strike or lockout could greatly affect both imports and exports in Canada. Importers and exporters looking to get cargo moving will need to resort to other modes of transport to move their goods. The CIRB will determine what essential services, if any, will be required to move if a stoppage of work goes into effect.

- 许多行业都会受到重大影响,包括严重依赖铁路运输货物的农业部门。

- 货物在国内的运输主要依靠转运和将货物用卡车运到最终目的地。然而,这些解决方案成本高、耗时长,对大多数进口商而言并非长期战略。CN 和 CPKC 都坚定地致力于通过谈判达成协议,防止任何停工事件的发生。

[Ocean - TPEB]

- 泛太平洋航线的运量依然强劲,超过了去年的水平。由于好望角航线(COGH)以及亚洲和北美的港口拥堵,我们的航班出现了结构性空白。由于好望角附近的天气状况,预计前往美国东海岸(EC)的航线将进一步延误,运力将面临挑战。

- 自从额外的装载机 (XL) 空间被注入泛太平洋贸易通道后,我们看到来自中国主要港口的美国西海岸 (WC),特别是太平洋西南部 (PSW) 的空间压力有所减少。

- 积极的一面是:巴拿马加通湖的水位已经恢复,当地政府也放宽了巴拿马运河的重量限制。

- 浮动运价:船公司继续下调至欧共体、西欧和墨西哥湾沿岸的即期运价,以满足供需。已宣布在 8 月下半月全面上调运价(GRI)。

- Fixed rates: Peak Season Surcharge (PSS) discussions are very intense at the moment, as the gap between FAK and NAC rates do not support mitigations, specifically in light of a potential GRI in August.

[Ocean - FEWB]

- THE Alliance announced three more void plans for September due to vessel delays, continuously impacting available capacity in the market.

- 与 6 月和 7 月的市场相比,8 月最后一周和 9 月初的需求略有放缓。浮动费率仍然偏高,而且还有空白船期,船位前景依然紧张。

- 长期指定账户业务仍然受到承运商空间和设备优先权的限制。

- 自 5 月和 6 月以来,设备短缺现象已有所缓解。对于一些直接挂靠较少的装货港 (POL),我们仍然预计某些集装箱类型(如 20'GPs)可能会出现设备短缺。

- 对于有目标交付日期的紧急货物,我们建议尽快选择高级选项,以获得更早的预计起飞时间(ETD)和设备优先级更高的舱位。

[Ocean - TAWB]

- 地中海和北欧的拥堵状况,加上船期可靠性问题和航班空白,导致 9 月 1 日的票价上涨。

- 德国东南部和腹地某些地区的设备短缺问题依然存在。到目前为止,预计德国港口不会再发生罢工。

- 最令人担忧的是美国可能发生的罢工。

- 为确保最顺畅的装船体验,我们建议北欧以外的预订提前 1-2 周预订,地中海以外在沿海港口装船的预订提前 2-3 周预订。

[海洋 - 美国出口]

- 从美国到印度次大陆、中东港口和北欧港口的运力紧张,这与船只缺失和空航有关。依靠支线服务前往最终卸货港(POD)的航线运力正在减少,因为适当的船只正在转向头程航线,而拥堵状况继续恶化支线航线的重复服务能力。

- Continual changes to earliest return dates (ERDs) present ongoing challenges for U.S. exporters.

- 为确保最顺利的装货体验,我们建议在沿海港口装货的客户提前 2 周预订,在内陆铁路点装货的客户提前 3-4 周以上预订。

[航空 - 全球]航空货运更新 2024 年 7 月 22 日(周一)至 7 月 28 日(周日)(来源:WorldACD

- 全球货运吨位保持稳定,地区之间存在差异:全球航空货运吨位在前一周下降-2%后,在七月的最后一周保持稳定,与六月底相比,总体下降-5%。全球六个主要地区中有四个地区的货运量出现下降,中美洲和南美洲下降了-4%,亚太地区、北美洲和非洲各下降了-1%。与此同时,欧洲和中东、非洲和南美洲分别增长了 +2% 和 +1%。

- 孟加拉国中断的影响:在第 28 周和第 29 周,由于政治抗议和互联网停电,从孟加拉国运往欧洲的吨位下降了 -29%。在第 30 周,货运量反弹了 6%。第 29 周和第 30 周的同比降幅都在 -50% 左右。

- 吨位同比增长趋势:第 30 周全球吨位同比增长 6%,仍低于 2024 年上半年 12%的平均水平。第 29 周和第 30 周合计的年同比增长率为 +7%,表明增长速度可能放缓。据初步估计,7 月份的环比增幅为 +9% 至 +10%。

- 航空货运费率:第 30 周,全球运价小幅下跌-1%,但两周运价保持稳定(2Wo2W)。与去年同期相比,运价上涨了 13%,其中东、南非地区(+55%)和亚太地区(+24%)涨幅较大。全球平均房价比 COVID 前的水平(2019 年 7 月)高出 +45%。

- 地区运价大幅上涨:亚太地区到美国的现货价格在第 30 周下降了-3%,但同比仍上涨了 62%。新加坡到美国的运价超过了每公斤 9 美元,是去年的两倍多。由于需求旺盛而运力有限,孟加拉、斯里兰卡、印度和迪拜的运价涨幅最高。

请与您的客户代表联系,了解货运所受影响的详情。

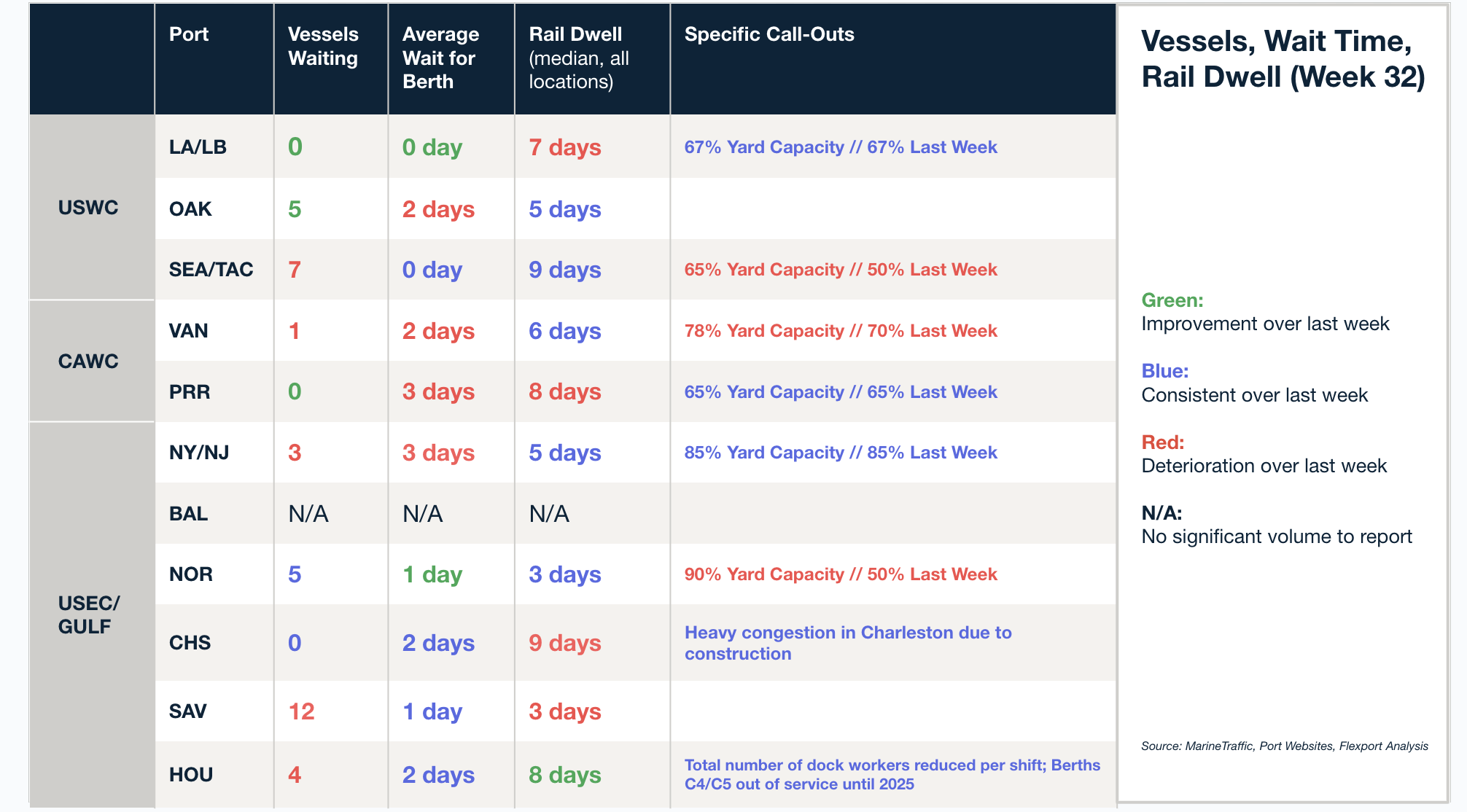

北美船舶停留时间

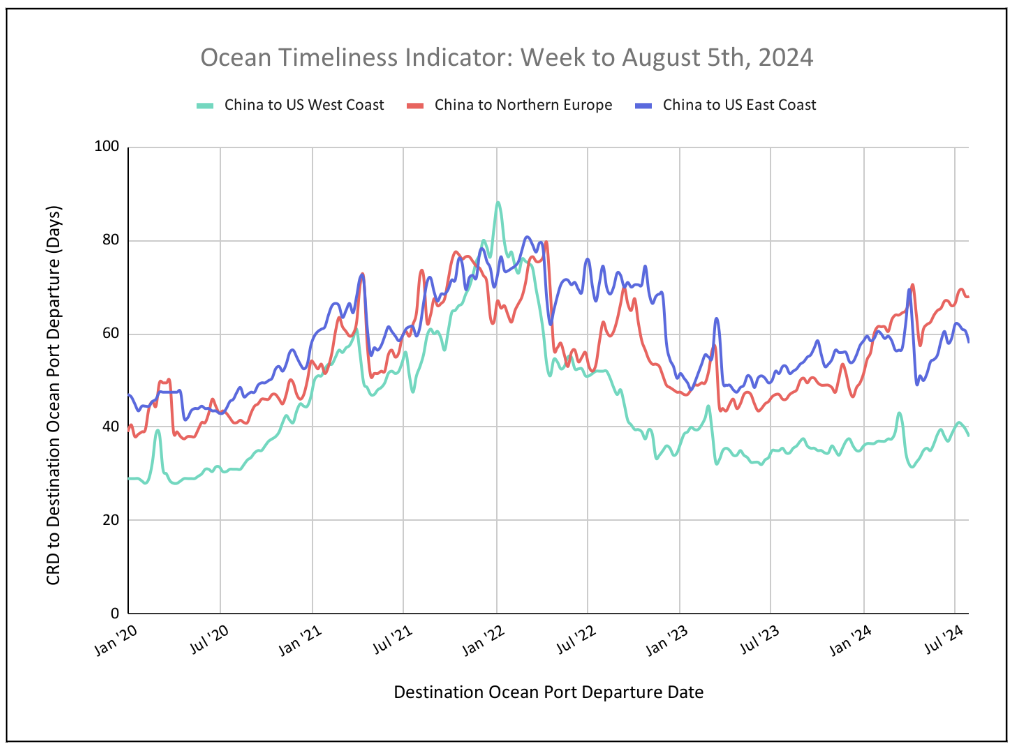

柔性海运及时性指标

中国至美国西海岸和中国至美国东海岸的海洋适时性指标保持下降趋势,中国至欧洲的海洋适时性指标保持稳定。

至 2024 年 8 月 5 日的一周

本周,中国至美国东海岸和中国至美国西海岸的"远洋及时性指标 "连续第三周加速下降,分别从60.5天降至58天和39.5天降至38天。

来源于 Flexport.com