Trends to Watch

- [Air – Global] Global air cargo tonnages have rebounded faster than in 2022 following the Thanksgiving holiday in the U.S., with a notable increase in tonnages and global average rates. Particularly, rates ex-Asia Pacific continue to rise strongly, especially trade lanes to North America and Europe. Year-on-year, global cargo volumes are up, driven primarily by a significant increase ex-Asia Pacific, while available capacity has also substantially increased across various regions compared to 2022. Despite a year-on-year decrease in worldwide average rates, they are still considerably higher than pre-COVID levels, reflecting ongoing strong demand and a market recovery in the air cargo industry.

- [FEWB – Ocean] Market demand is moving up in December and ships are filling up. As the rate gap between long-term deals and the spot market is widening, the long-term deal space was largely impacted by the carriers due to serious bleeding over the past few months. Thus, a significant peak season surcharge is expected before the Lunar New Year. Blank sailings in December are less than 10% per week (excluding the service suspension of FE5 by The Alliance that impacts the Southeast Asia export). We expect rates to continue climbing as we approach the second half of December and there is a high likelihood that another wave of GRIs effective first of January will reflect the pre-Lunar New Year rush demand. In other news, the Antwerp operation was partially impacted due to last week’s strike (roughly 49 ships were impacted as a result), which has already resumed full operation this week. Plus, ONE Orpheus (FP1 service calling Asia-NEUR at the moment) struck a bridge during its transition in the Suez Canal. The inspection has finished and the vessel is currently at the shipping yard for temporary repair. MED trade: Following North Europe, MED GRI is also thriving in December supported by the strong demand. However, space is very tight at the moment as we observe a cargo rush before the Lunar New Year. As in North Europe, there is a high likelihood that another wave of GRI effective first of January will reflect the pre-Lunar New Year rush demand. Similarly, the EU Emissions Trading System is going to apply effective the first of January, but so far we don’t see any mitigation of this surcharge by carriers.

Please reach out to your account representative for details on any impacts to your shipments.

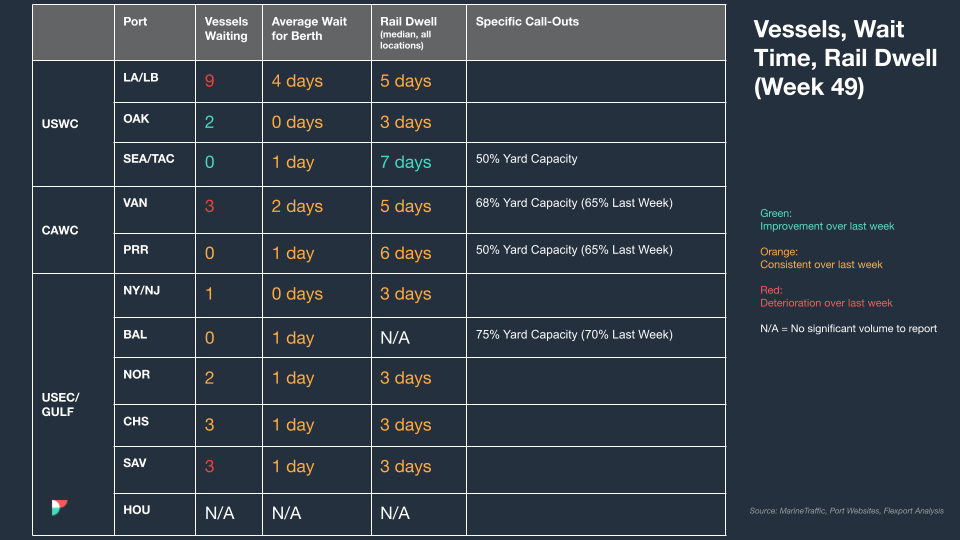

North America Vessel Dwell Times

This Week In News

Supply Chain Coalition Presses Background Check Reform

A coalition of supply chain stakeholders, including the American Trucking Associations (ATA), is urging Congress to quickly pass the Transportation Security Screening Modernization Act. The legislation aims to eliminate redundant background security checks for essential workers such as truck drivers, creating a streamlined, one-stop process for obtaining credentials like the Transportation Worker Identification Credential, Hazardous Materials Endorsement, and TSA PreCheck. Approximately 140 signatories, representing various sectors, argue that subjecting workers to duplicate checks for different credentials from the same agency is inefficient and burdensome.

Carriers Pushing Rate Hikes Ahead of New Year Service Suspensions

To improve rates on the Asia-Europe trade route, Hapag-Lloyd and CMA CGM have increased their FAK rates for 40ft containers from Asia to North Europe to $3,000 starting January 1, 2024. Despite this, the Drewry WCI Asia-North Europe rate remains at $1,343 per 40ft. Hapag-Lloyd’s rate for West Mediterranean ports will be $3,200, $200 higher than CMA CGM’s proposal. Other carriers are expected to follow suit.

The Logistics Sector Was Weak in November, but That’s Not Necessarily Bad News

The latest Logistics Managers’ Index reveals a weakened state of the shipping industry in November, with the index experiencing its most significant fall since April 2022. Unlike the concerns around excess inventory last year, the current weakness is less alarming as it stems from reduced inventory levels due to heightened consumer buying during events like Thanksgiving, Cyber Monday, and Black Friday. Experts suggest that as supply chains stabilize, retailers are maintaining leaner shelves, contributing to lower warehousing storage costs. The emphasis is now on improving efficiency in the logistics sector through investments in technologies like electric delivery vehicles and artificial intelligence for enhanced inventory management, rather than expanding inventory levels.

Source from Flexport.com