It is an irony of container shipping, well established over the course of decades, that actions available to carriers to protect their profitability almost always accrue to the disadvantage of their customers. And yet carriers take the action anyway.

It’s looking like that will be no different in 2024.

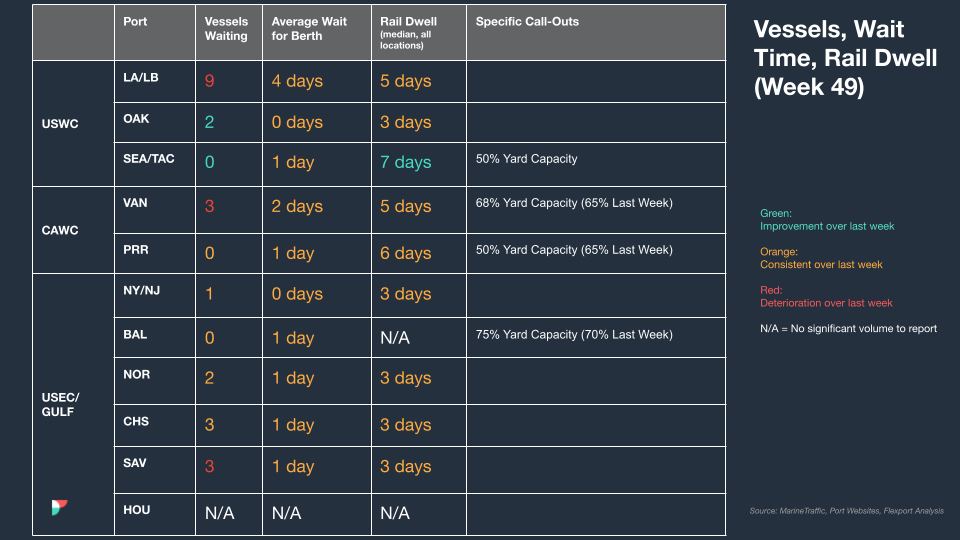

The year 2023 completed the extreme up and down arc of most metrics in this market — but not all. Rates, carrier profits and port congestion all normalized. “Vessels and cargo arriving, departing and shifting around the ports of [Los Angeles and Long Beach] continue to move normally with no labor delays,” Kip Louttit, executive director of the Marine Exchange of Southern California, said on Dec. 9.

That’s a far cry from two years ago when over 100 container ships waited outside the ports for a berth and trans-Pacific spot rates were over $10,000 per FEU.

But even with ports clear of congestion, service reliability remains an outlier, not having reverted to pre-COVID levels. And because of overcapacity and carriers’ aggressive response, it will likely not return to normal levels in 2024. That will put pressure on those shippers who were hoping to return to the days of low-cost leaner inventories, especially amid higher interest rates, based on supply chains premised on predictable ocean transit times.

Unfortunately for shippers, that is nowhere in the picture. Global container ship scheduled reliability stood at 64.4% in October, up from 51.8% a year earlier and approximately 35% in 2021. But the October figure was still 15 percentage points below 2019 levels, and with no sign of improvement since May, according to Sea-Intelligence Maritime Analysis.

New vessels worsen overcapacity

To manage the impact of overcapacity, now a reality for the next two to five years depending on who you ask, carriers are pulling out all the stops to absorb capacity. They have many tools at their disposal, whether it’s blank sailings, spontaneously adding port calls, further slow steaming, laying up ships or taking longer routes. While all that will combine to help carriers weather a rough patch of unfavorable supply-demand economics, it undermines schedule integrity and any semblance of service reliability.

“These oversupplied conditions are expected to persist for the next three to four years, primarily driven by the influx of newly ordered vessels entering the market,” said Christian Sur, executive vice president of Unique Logistics.

The pain doesn’t end there. As new and larger ships hit the water, the trend is toward larger tonnage being deployed on key trade lanes. Several sources have commented to the Journal of Commerce on the growing evidence of mega-ship concentration at the larger ports.

“Larger container ships and liner network optimization will accelerate concentration of cargo on to fewer ships calling gateway ports,” said Griff Lynch, executive director of the Georgia Ports Authority.

“We expect the frequency of larger container vessel calls to continue to increase as shipping lines work to decrease their carbon intensity,” said Capt. Allan Gray, president and CEO of the Halifax Port Authority. “The larger, newer vessels are more efficient, which means carbon intensity per container is lower.”

Those ships drive down CO2 per container and help carriers achieve more favorable treatment under the International Maritime Organization’s (IMO’s) Carbon Intensity Index (CII) efficiency rules, while positively impacting shippers’ Scope 3 emissions. For shippers, it still means what big ships have always meant: benefits that roll up more to the carrier than to themselves.

The reality of larger ships

Big ships mean longer port calls, surges at ports, more time needed to get containers unloaded and made available to consignees, more cargo concentrated on fewer ships, and fewer port calls. That transfers the pressure to ports and port ecosystems to effectively manage regular surges.

“Larger ships generally mean higher box exchanges,” said Dean Davidson, head of maritime advisory at Infrata. “Loaded Asian imports will remain the dominant activity at major US and Canadian ports and pressure will remain on these gateways to get the containers moved onto the next leg of the supply chain, whether its trucking, rail, transloading or onward distribution.”

The risks are further compounded by the potential clash of pared-back capacity set against the possibility of a surprise acceleration in cargo growth, which is rarely, if ever, predicted. Also hovering is the ever-present potential for another unpleasant shock, whether from geopolitics, severe weather, a public health crisis, a cyberattack or some other menace yet to be identified.

“Despite the unprecedented level of turmoil experienced in overcoming challenges over the past several years, it is only the warning shot for what is to be the most industrywide disruptions still to come,” said Cosco Shipping Lines Executive Vice President Paul Nazzaro.

This all rolls up to an environment of heightened risk for shippers as 2024 begins.

Source from JOC.com