Trends to Watch

Talking Tariffs

- U.S. and India Announce Trade Deal: On February 2, the U.S. and India announced a trade agreement that will reduce the total effective duty rate on Indian goods from 50% to 18%. While President Trump stated that the agreement would take effect immediately, he has yet to issue an executive order or Federal Register notice implementing the deal. Provisions of the agreement include:

- The U.S. will lower its 25% reciprocal tariff rate on Indian goods to 18%. The U.S. will also remove the additional 25% tariff on Indian goods imposed last August in response to India’s purchases of Russian oil.

- India will eliminate tariffs and non-tariff barriers on U.S. goods.

- India will halt purchases of Russian oil, and purchase “much more [oil] from the United States and, potentially, Venezuela.”

- India will purchase over $500 billion’s worth of U.S. energy, technology, agriculture, and coal products.

- Electronic Refunds from U.S. Customs and Border Protection (CBP): Tomorrow (February 6), CBP will begin issuing all refunds electronically. CBP will no longer issue checks for refunds, except in limited circumstances.

- CBP has published FAQs related to the upcoming transition.

- Importers should confirm access to their Automated Commercial Environment (ACE) Portal account and set up electronic refunds as soon as possible.

- Check out our blog for instructions on applying for an ACE Portal account, a step-by-step guide to setting up electronic refunds, and guidance for foreign importers of record.

- European Parliament Unfreezes Approval of EU-U.S. Trade Deal: On February 4, the EU agreed to unfreeze its approval of the trade agreement that it struck with the U.S. last summer. While the U.S. implemented a minimum total tariff of 15% on EU goods last August, other provisions of the trade agreement remain under EU legislative review and have yet to take effect. With the freeze now lifted, EU lawmakers may vote on the trade agreement as soon as February 24.

- The EU had suspended its approval of the trade deal last month, after President Trump announced plans to impose a 10% tariff on eight European trading partners due to a perceived lack of cooperation in his quest to purchase Greenland. However, after striking a deal framework on Greenland with NATO, President Trump later called off those tariff plans.

- Potential Tariffs on Nations Providing Oil to Cuba: On January 29, President Trump issued an executive order laying the groundwork for potential tariffs on nations that “directly or indirectly sell or otherwise provide any oil to Cuba.”

- Per the order, the Secretary of Commerce and other Cabinet members will first identify all nations supplying oil to Cuba. Afterwards, if they determine that the U.S. should proceed with the tariff, they will advise President Trump on a potential duty rate. The timeline for these processes is currently unclear.

- Mexico was the biggest supplier of oil to Cuba in 2025, accounting for about 44% of Cuba’s total crude imports. Other current suppliers include Russia and Algeria. While Venezuela was previously Cuba’s largest supplier, its oil exports to Cuba dropped sharply in 2025 due to sanctions and infrastructure challenges, and recently ceased altogether following the U.S. capture of Venezuelan President Nicolás Maduro.

- While Mexico recently paused oil shipments to Cuba due to supply fluctuations, Mexican President Claudia Sheinbaum stated earlier this week that her nation would send humanitarian aid to Cuba. The ongoing energy crisis in Cuba has grown increasingly severe in recent months, with some reports indicating that the country’s current reserves will last only 15 to 20 more days.

- U.S. Signs Trade Deals with El Salvador and Guatemala: Both trade agreements will eliminate reciprocal tariffs on exports to the U.S. that comply with the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR), and on select goods that cannot be produced in the United States. It is unclear exactly when these trade agreements will be implemented.

- A Potential Tariff on Canadian Aircraft: In a January 29 Truth Social post, President Trump announced plans to impose a 50% tariff on all Canadian aircraft if Canada does not certify American-made Gulfstream planes.

- The announcement comes amid mounting trade tensions between the U.S. and Canada. Last month, President Trump indicated that he would levy an additional 100% tariff on Canadian goods if Canada made a trade deal with China. Soon after, Canadian Prime Minister Mark Carney denied any plans to move forward with a China trade deal.

- Other Recent Developments:

- On January 27, the EU and India announced a landmark trade deal that will reduce or eliminate duties on nearly all bilaterally traded goods over a phased period of several years. Among the impacted goods are EU-origin cars: India will gradually reduce its 110% duty rate on EU motor vehicles to 10%, applicable to an annual quota of 250,000 EU vehicles. The trade agreement is expected to take effect by the end of 2026.

- Given that the Korean legislature has not approved the trade agreement terms that the U.S. and Korea agreed upon last July and finalized last October, President Trump announced that he intends to raise reciprocal tariffs on Korea and Section 232 tariffs on Korean autos and lumber from 15% to 25%. President Trump has yet to confirm these duty increases via executive order or Federal Register notice.

- The EU announced last week that it would extend the suspension of its countermeasures against the U.S., postponing retaliatory tariffs on €93 billion (about $109 billion)’s worth of U.S. goods for an additional six months. The EU’s existing suspension of these countermeasures expires this week.

- Find the latest tariff and trade developments on our live blog.

We recently launched the Flexport Tariff Refund Calculator to help businesses scenario-plan ahead of the U.S. Supreme Court ruling on IEEPA tariffs. Instantly calculate total duties that are potentially eligible for refunds, break them down by duty category, and quickly understand your potential return if the Supreme Court orders refunds.

Ocean

TRANS-PACIFIC EASTBOUND (TPEB)

- Capacity and Demand:

- To start February, capacity is holding at 85-88% until Lunar New Year. However, a blank sailing period related to Lunar New Year capacity adjustments is expected to begin in the last week of February and continue through the first half of March.

- Volumes have remained steady since the December holiday season. This year’s pre-Lunar-New-Year rush—which has been pushed ahead by 3 to 4 weeks—has been “spread out,” partially due to the late holiday this year, in contrast to the sharp volume spikes seen in previous years. We have not seen any further uptick in volumes.

- We are seeing some signs of cargo rollings as carriers tighten their rolling pool in preparation for Lunar New Year and blank sailings.

- Freight Rates:

- All carriers have withdrawn the February General Rate Increase (GRI), while mitigating rates. These rate mitigations are beginning to slow down as we near Lunar New Year.

- Carriers have confirmed and pushed Peak Season Surcharges (PSSs) to March. With Lunar New Year just over a week away, these actions indicate a lack of “peak pressure” in the current market.

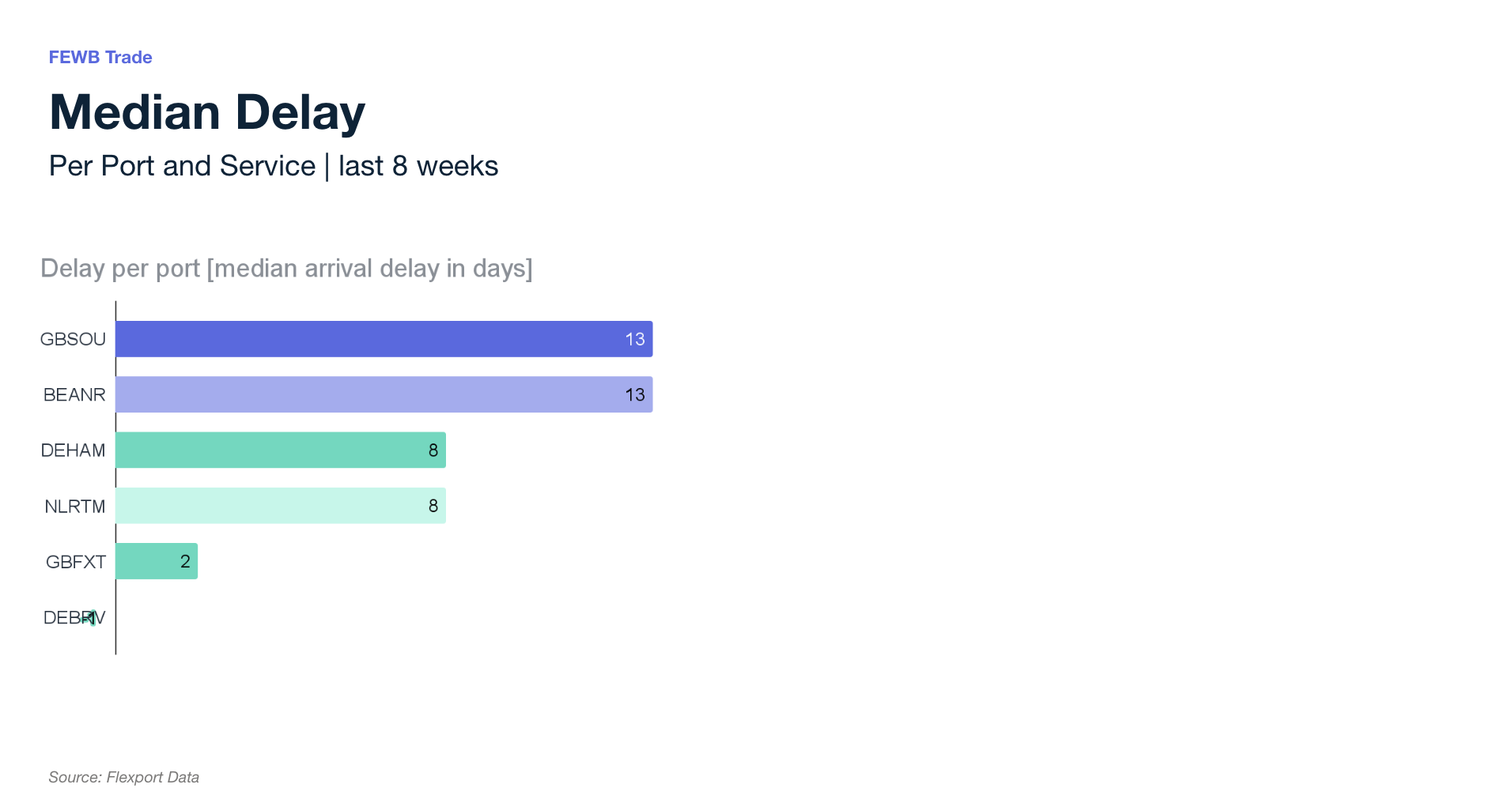

FAR EAST WESTBOUND (FEWB)

- Capacity and Demand:

- The market has officially entered the pre-Lunar-New-Year “quiet period.” Spot demand is rapidly decelerating, as the final urgent shipments have departed. Factory production in China is beginning to wind down.

- To counter the demand dip, carriers have implemented aggressive blank sailing programs for February. The focus has shifted entirely from moving peak volumes to managing utilization. Carriers are actively building rolling pool at transshipment hubs like Singapore to ensure sufficient load factors during upcoming blank sailings.

- Operations at Asian Hubs:

- Despite the drop in demand, equipment availability remains tight for 40’ HC containers in Shanghai and Ningbo as shippers rush to clear floors before the holiday break.

- Congestion in Singapore remains elevated due to rolling pool strategies, with dwell times around 7 days.

- Operations in Northern Europe: Operational fluidity remains severely hampered by winter weather. Amid ongoing adverse weather risks, we are continuously monitoring the situation and taking immediate measures to ensure safe and smooth operations.

- Main yard utilization at Rotterdam: ECT, 80%; Rotterdam World Gateway (RWG): 85%; Delta II: 50%; Maasvlakte II (APMT MVII), 95%.

- Main yard utilization at Hamburg: HHLA Container Terminal Altenwerder (CTA), 85%; Eurogate Container Terminal (CTH), 100%.

- Rail backlogs in Germany persist, delaying hinterland evacuation by 4 to 6 days.

- Freight Rates:

- The Shanghai Containerized Freight Index (SCFI) continues to trend downward, recording mild-to-moderate declines. Rates are approaching a “soft landing” that significantly exceeds historical averages, supported by Cape of Good Hope routings and capacity management.

- Heavy blank sailings in Weeks 7 through 9 are creating an artificial floor, preventing rates from collapsing despite lower demand. Compared to pre-pandemic levels, the trading environment is expected to remain stable but expensive.

- Shippers should anticipate a tight space situation during the post-holiday period in early March. As factories reopen, reduced capacity due to blank sailings will likely result in a sharp, short-term spike in competition for space, potentially hardening rates again for the second half of Q1.

TRANS-ATLANTIC WESTBOUND (TAWB)

- Capacity and Demand:

- North Europe and West Mediterranean: Heading into early February, demand has moderately firmed. This is supported by record tonnages, despite heavy blank sailings keeping volumes below peak levels.

- East Mediterranean: Demand is relatively stronger.

- Equipment:

- Critical container and chassis shortages persist into early February, especially in Austria, Slovakia, Hungary, Southern and Eastern Germany, and Portugal. This has necessitated earlier cut-offs and flexible pickups.

- Freight Rates:

- Heading into early February, rates are holding stable across North Europe, the East Mediterranean, and the West Mediterranean. Spot levels to the U.S. East Coast are generally within the low-to-mid $1,500/FEU range.

- CMA CGM has filed a limited Peak Season Surcharge (PSS), while other carriers are holding back amid competition.

INDIAN SUBCONTINENT TO NORTH AMERICA

- Capacity and Demand:

- Given the U.S.-India trade deal announced earlier this week, the market is expecting an uptick this month. While the reduced tariffs have yet to officially take effect, the market anticipates an increase in volumes from India to the U.S.

- To the U.S. East Coast: CMA CGM (INDAMEX) and Maersk (MECL) continue to proceed with Suez routings through the Red Sea. Capacity is available, but the upcoming tariff mitigation will likely rebalance capacity and demand.

- To the U.S. West Coast: Capacity on PS3, the sole direct service from India to the U.S. West Coast, is available. As demand potentially increases, feeders that connect to main strings to bring containers to the U.S. West Coast may begin to grow constrained.

- Freight Rates:

- To the U.S. East Coast: As we enter February, rates are being reduced. If demand increases as anticipated in response to the tariff mitigation announcement, rates are likely to increase into March.

- To the U.S. West Coast: Rate levels remain low into February, but may bounce back if demand rises.

Air

- North China:

- The market is undergoing an uneven recovery. Demand is strengthening on Chicago (ORD) and New York (JFK) lanes, driven by general cargo bookings. Meanwhile, other U.S. gateways remain flat.

- Rate movements mirror this trend, with upward pressure on ORD and JFK.

- The absence of broad momentum suggests a muted pre-Lunar-New-Year peak, especially as some suppliers prepare for early workforce releases.

- South China:

- The market is preparing for the holiday peak, though demand is expected to soften as factories begin closing next week.

- While capacity remains stable for now, flight cancellations are expected during the holiday period.

- Taiwan:

- Demand remains stable, but rates are increasing due to severe backlogs related to recent weather disruptions in the U.S.

- Vietnam:

- Market demand has picked up slightly ahead of Lunar New Year, resulting in higher rates on Trans-Pacific Eastbound lanes.

- Carriers are continuing to work through backlogs related to last week’s severe weather in the U.S.

- Cambodia:

- The market is currently stable. However, rates are expected to edge higher as factories accelerate production.

- Operations will remain normal during the holiday.

- South Korea:

- Backlogs from last week’s storms in the U.S. are expected to persist through this week.

- Bookings for all U.S. destinations are fully booked into early February, with slight rate increases.

- Malaysia:

- Demand on Trans-Pacific Eastbound lanes remains stable, with firm rates.

- While capacity is generally adequate, congestion has been reported at major hubs for connections into Dallas (DFW), Atlanta (ATL), New York (JFK), and Los Angeles (LAX).

- Thailand:

- Demand at the end of January was weaker than expected, though volumes are anticipated to rise slightly before the holiday.

- Tight connecting space to the U.S. East Coast remains a challenge due to storm recovery.

- India:

- Market rates are gradually increasing as demand picks up, particularly on Trans-Pacific Eastbound lanes.

- Adverse weather has led to several flight cancellations. Shippers are advised to secure early pre-bookings to ensure space.

- Bangladesh and Pakistan:

- Capacity is available, but inquiries are rising due to the pre-Lunar-New-Year rush. For urgent shipments, shippers are encouraged to pre-book 4 to 5 days in advance.

(Source: Flexport)

Please reach out to your account representative for details on any impacts to your shipments.

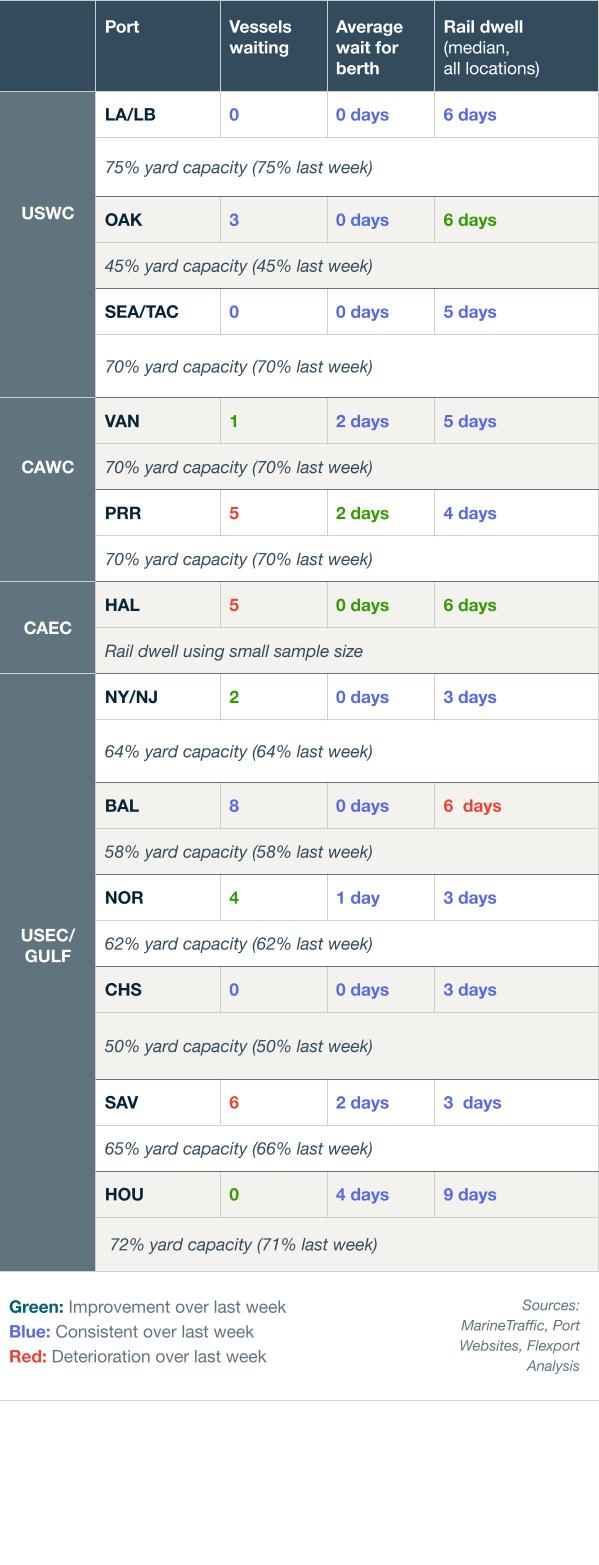

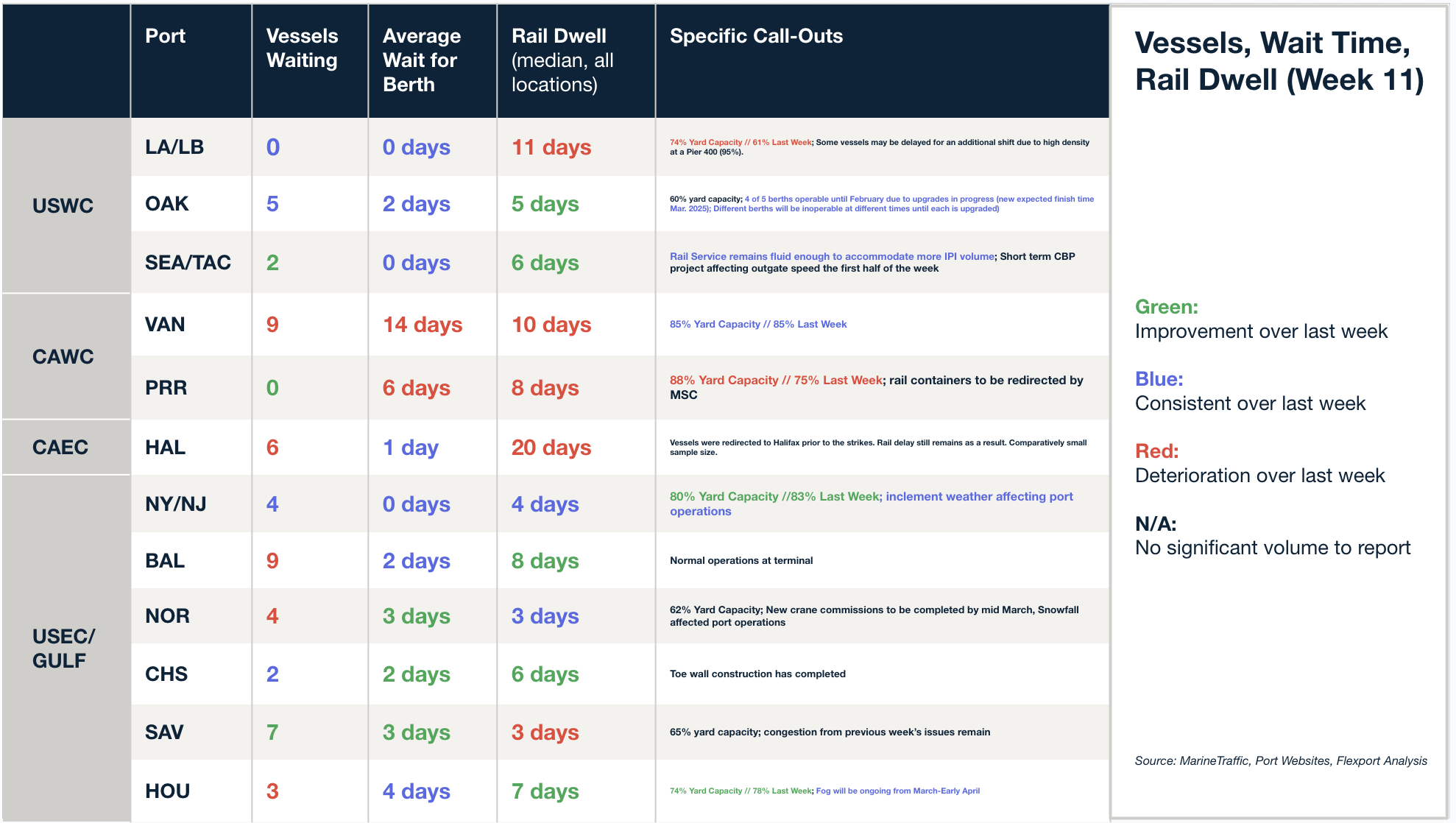

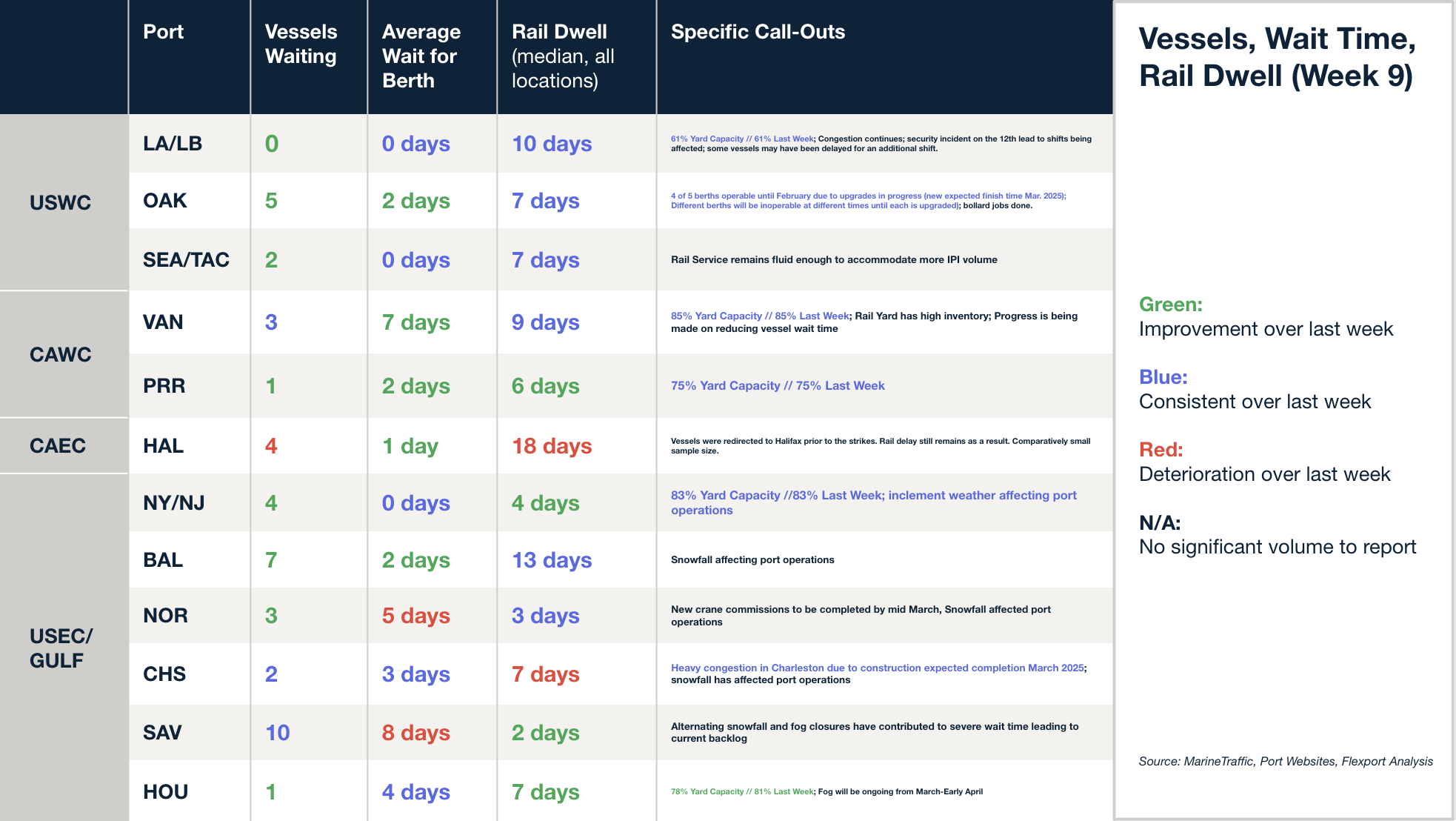

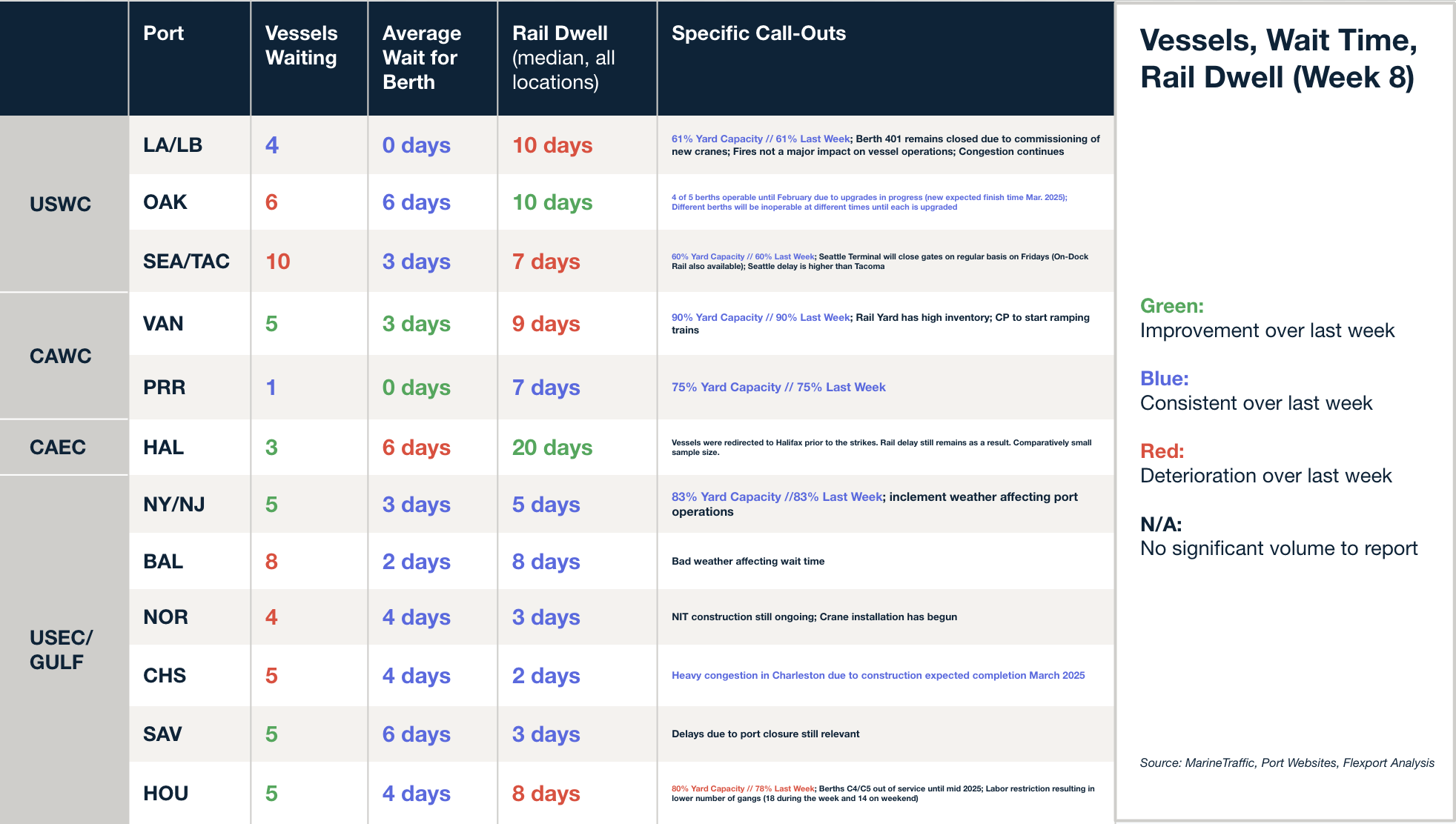

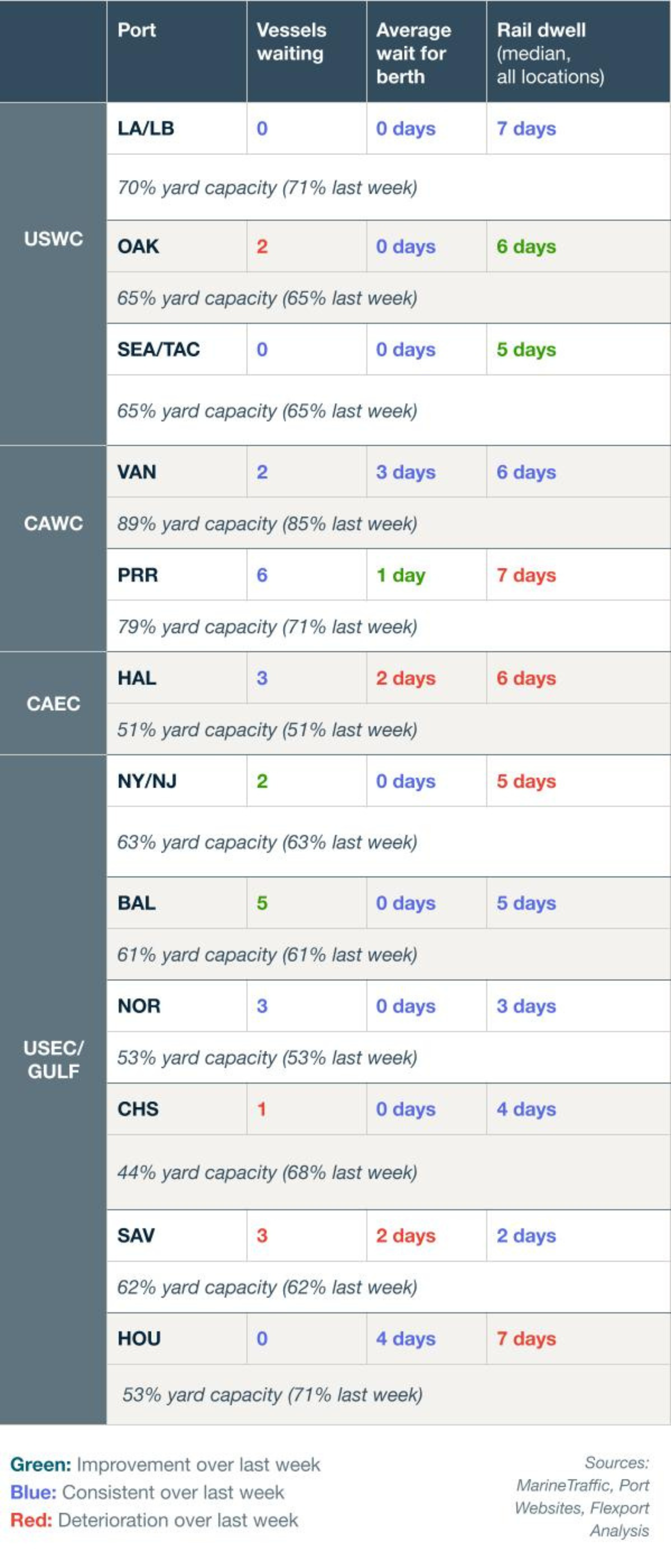

North America Vessel Dwell Times

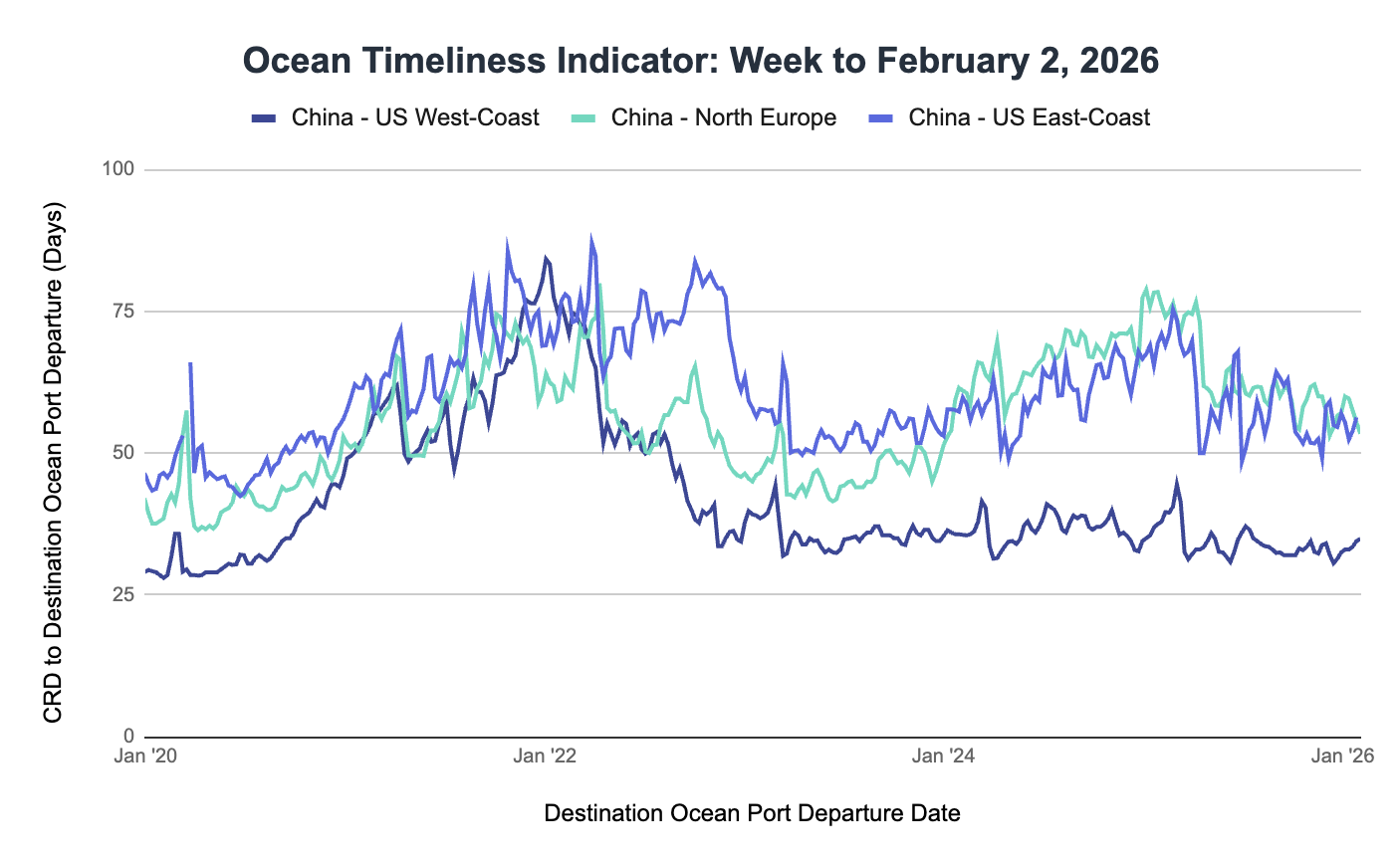

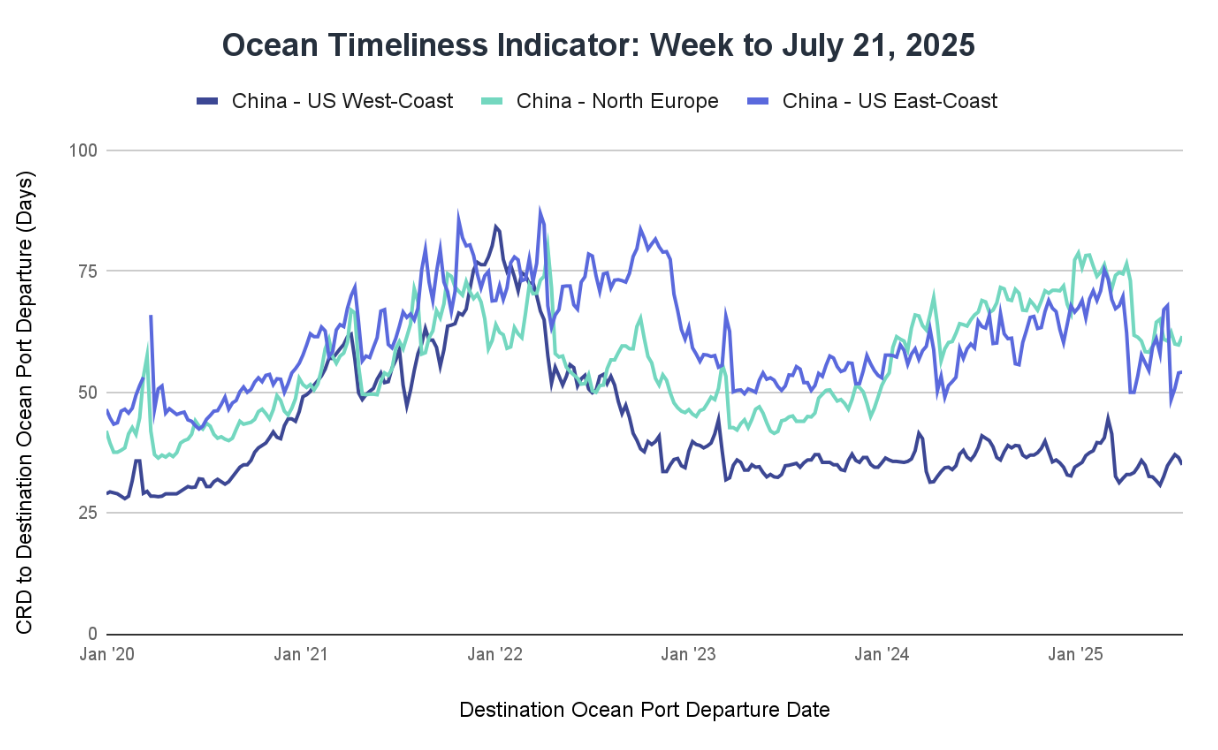

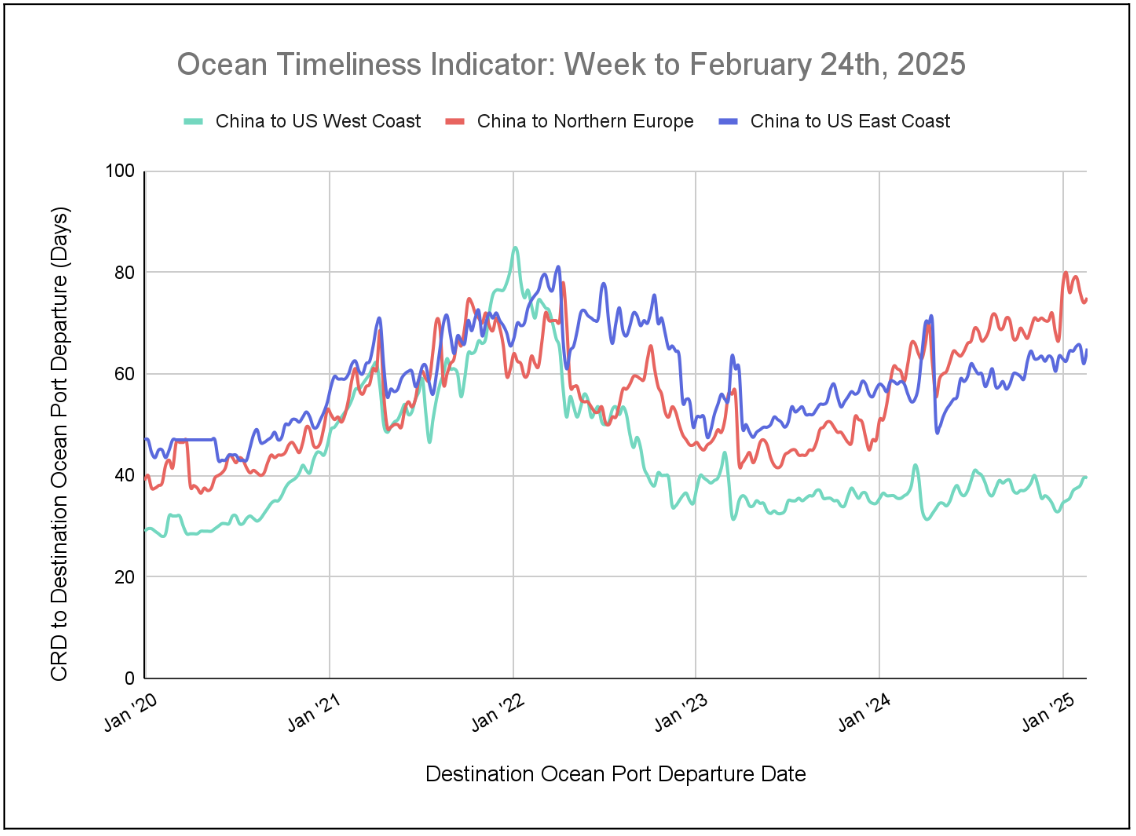

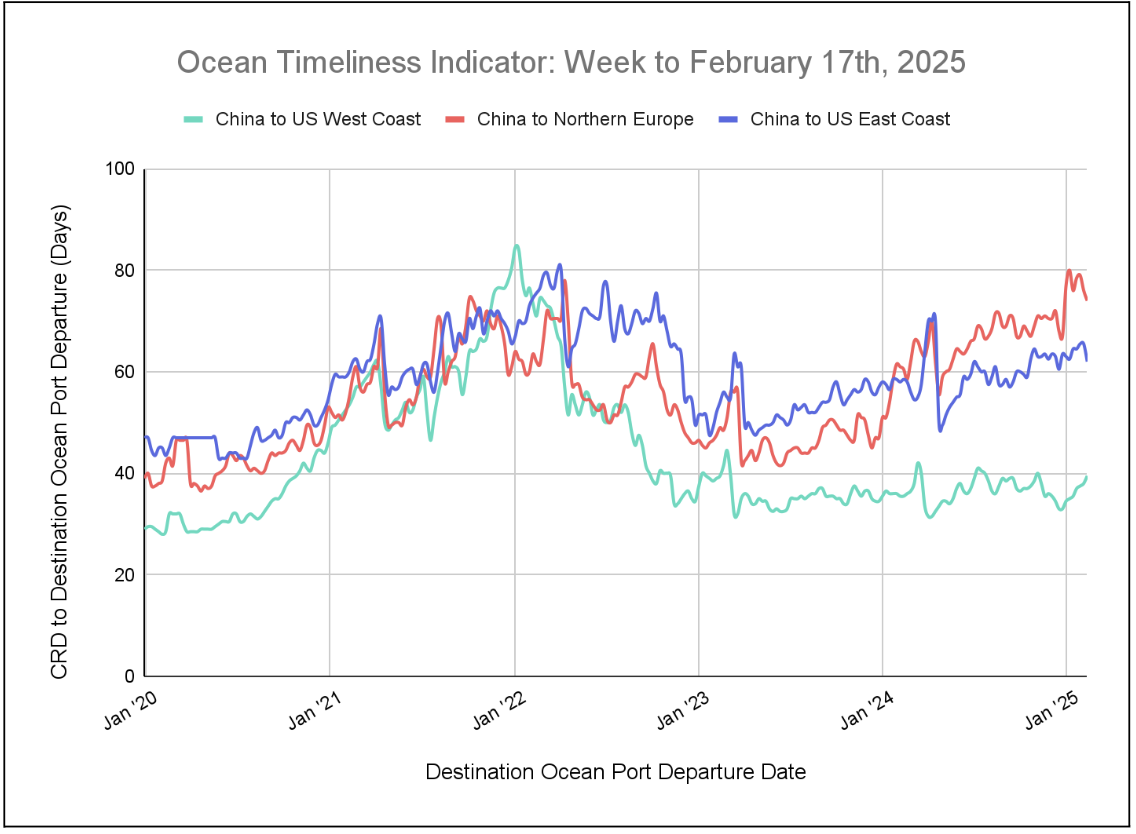

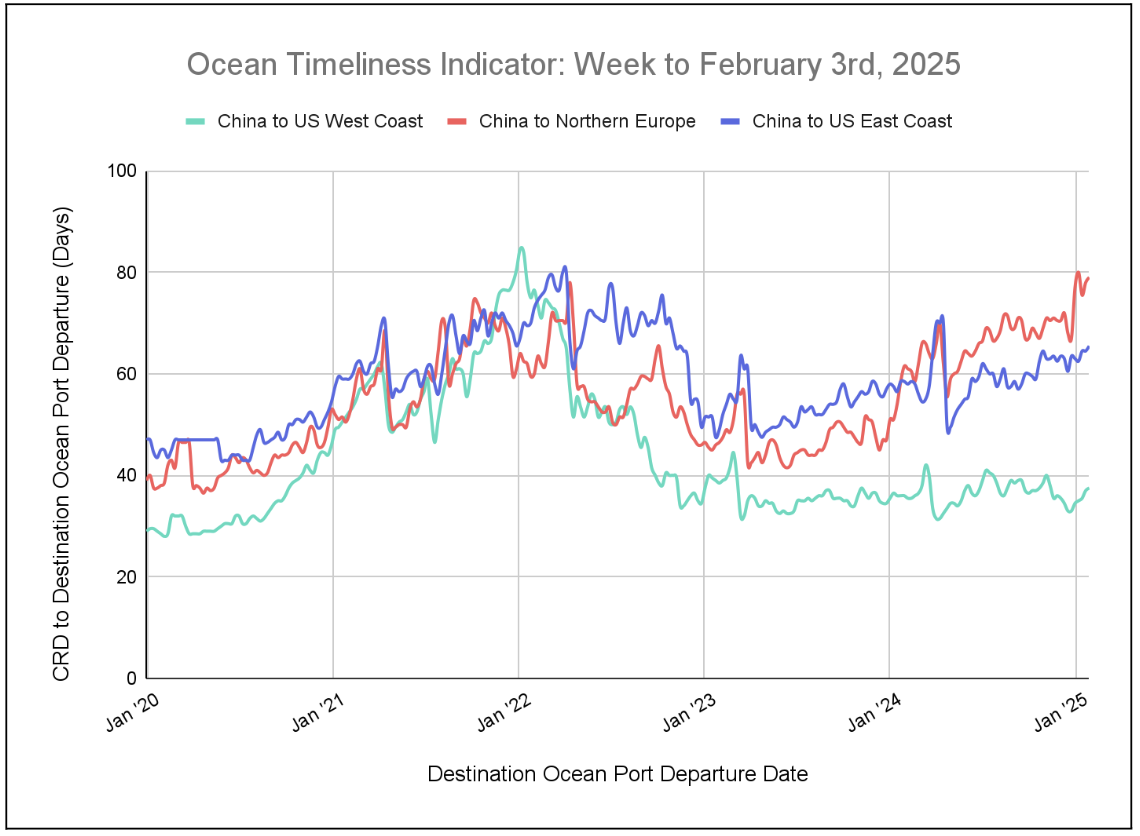

Ocean Timeliness Indicator

Transit time increased from China to the U.S. West Coast and China to the U.S. East Coast, and decreased from China to North Europe.

Week to February 2, 2026

Transit time increased from 33.5 to 34.5 days from China to the U.S. West Coast; increased from 53.9 to 56.3 days from China to the U.S. East Coast; and decreased from 57.5 to 55.4 days from China to North Europe.